The Quiet Shift: PMs No Longer Control Product Truth, Memory Markets Do

When supply constraints move faster than roadmaps, the job stops being about what to build and starts being about what you're allowed to ship.

It’s Tuesday morning in a product review meeting. A PM from a major laptop manufacturer pulls up the Q3 roadmap. The 16GB base configuration for their flagship ultrabook. The one they’ve been planning around for eight months. It maps to a certain margin target. A certain price point. A certain competitive story.

Then the supply team slides in a note from their chip vendor: DRAM prices just spiked 18% in the spot market.

The base model config now costs more to produce. The vendor isn’t reducing allocation. They’re not being flexible on timeline. They’re raising the price per gigabyte because they can, because everyone needs memory, and because capacity is flowing upmarket first.

The PM has a choice now that isn’t really a choice.

Reduce the base memory

Raise the price

Change the architecture

Cancel the launch window

All of these break something that was already committed. The roadmap hasn’t changed. The market hasn’t changed. But the feasible frontier just collapsed inward.

This is not a unique situation anymore. It is becoming the operating environment.

The industry spent the last decade in a commodity memory cycle.

Prices fell. Capacity grew. Specs climbed without friction. A PM could plan around stable component costs. You could say “we want this device to have 16GB” and assume that would remain affordable through the product lifecycle.

That era is ending.

What changed is not the consumer demand for devices. It is the economics of producing them.

Samsung, SK Hynix, Micron. The three companies that control the vast majority of global memory production have quietly shifted strategy. They are no longer optimizing for volume. Samsung’s Q1 2024 earnings report showed their memory division returned to profitability not through cheaper capacity, but through higher average selling prices. Content-per-box increased.

Capacity allocation shifted toward high-density DDR5, HBM for AI servers, and premium NAND. The message from the industry was unspoken but clear: we are going to keep base-tier margins thin and push growth into premium configurations.

PM teams are only starting to feel this. But the math is simple. If your bill of materials just increased by 15-20% on core components, and your market won’t tolerate a 15-20% price increase, then you have a gap. You fill that gap by either accepting lower margin, raising price anyway, or finding a new constraint to optimize against.

Apple is already doing this. The iPhone 16 base model moved from 128GB to 256GB of storage. Apple hasn’t publicly explained the reasoning, but the supply economics suggest what likely happened: the cost of flash memory pricing shifted in a way that made increasing the floor spec cheaper per device than absorbing the cost in margin. The feature looked like value-add. It was, functionally, constraint accommodation.

This is the quiet part. When margin gets squeezed by upstream economics, you can’t just announce “we absorbed higher costs.” You have to reframe the problem as a product decision. Increase RAM. Add storage. Include a higher-tier processor. Make the specs look like progress when they’re actually distributed cost management.

The second-order effect is what gets to most PMs: they no longer control the feasibility calculus.

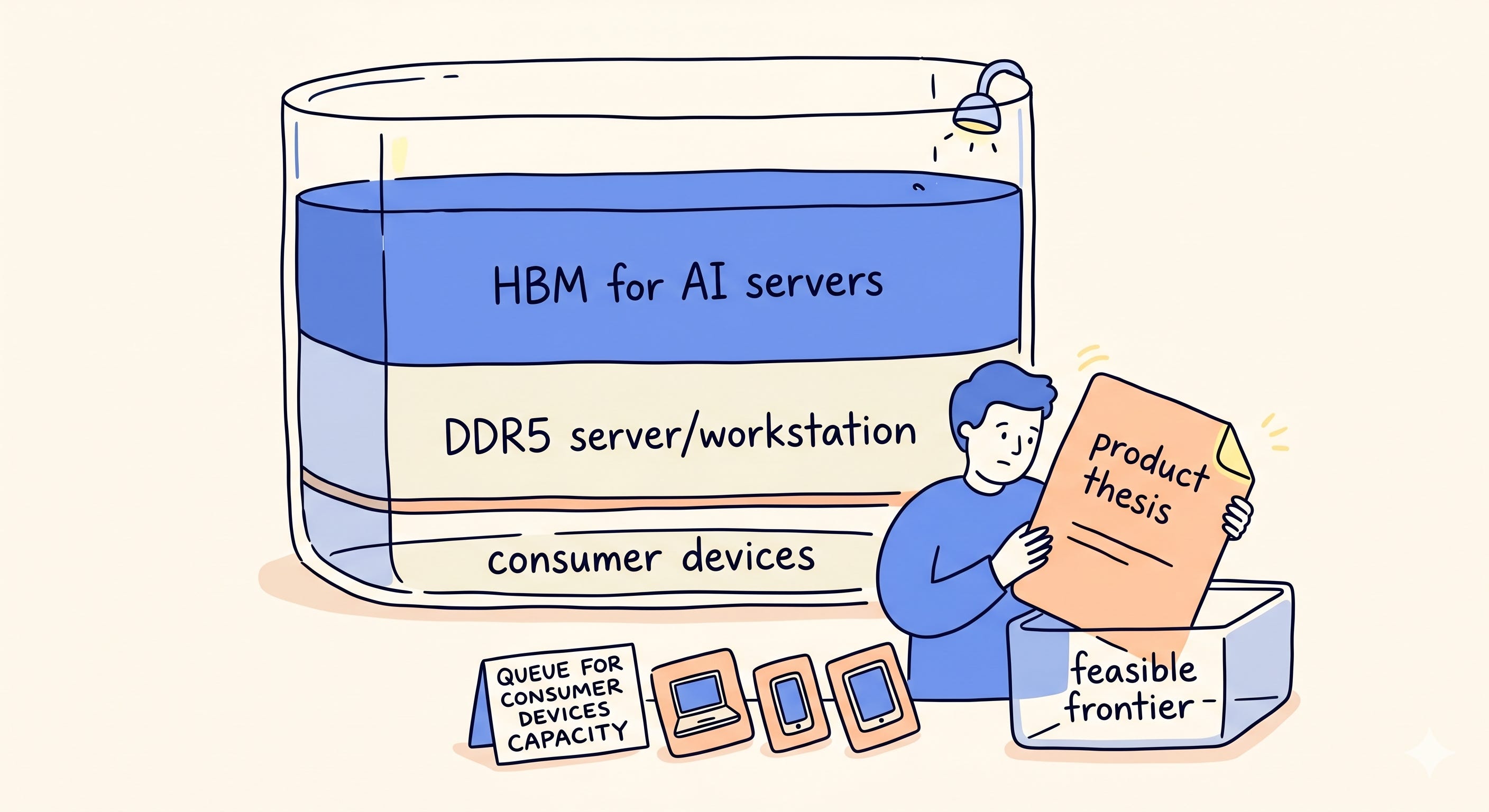

Five years ago, a PM could say “our thesis is that people want smaller, lighter devices with longer battery life.” That thesis could actually drive component choices. Supply teams worked backward from that vision.

Now the equation is inverted. Memory supply is allocated to HBM first (because AI infrastructure margins are infinite right now). Then DDR5 server and workstation capacity. Then the remaining allocation trickles down to consumer devices. The PM still has the thesis. But the thesis now has to fit inside a container whose size is determined by upstream capacity allocation.

This forces difficult choices that most product strategy frameworks don’t anticipate.

If you can’t get cheap base-tier memory, you have to pick:

Do you segment more aggressively (create a lower-spec model at a lower price)? Do you absorb the cost (reduce margin)?

Do you raise price (risk losing customers)? Do you redesign the architecture (delay launch)?

Do you lean into premium tiers only (cede the mainstream market)?

Each choice is a constraint choreography disguised as strategy.

The tier architecture becomes a financial instrument. Suddenly the difference between 8GB, 12GB, and 16GB is not a product hierarchy. It is a margin optimization vector.

The upgrade paths from base to plus to pro are no longer about feature differentiation. They are about spreading customers across a cost curve that their memory vendor has rewritten overnight.

Upgrade mechanics that felt like natural product thinking become supply-chain leverage.

Users don’t see the upstream constraint. They see the price jump and have to justify it to themselves through performance narratives that their PM team then has to construct.

This is not a short-term disruption. This is a structural reordering of how product gets made at companies that depend on memory-intensive components.

The companies feeling this hardest are the ones without direct supply agreements or scale large enough to force vendor behavior. The laptop OEMs working with fixed supplier allocations. The mid-tier phone manufacturers dependent on spot market purchases. The companies that thought product success alone created leverage.

Turns out, product success is downstream from supply agreement success. If Dell, HP, or Lenovo can’t secure the same memory allocation Apple does, their product teams inherit different constraints. Their base models carry different economics. Their upgrade incentives get rewired differently.

Apple’s advantage is not strategy anymore. It is purchasing power. They can pre-commit to HBM volumes. They can make memory vendors invest capex in high-capacity fabs. They can negotiate pricing that the rest of the industry simply can’t match. Right now, the best PM work at Apple isn’t happening in product strategy sessions but is happening in supply negotiations.

What gets me about this shift is the invisibility of it.

A user sees a 16GB base model and thinks “this company values giving me more memory.” The PM knows the truth is more complicated. The supply team knows it is actively complicated. But the narrative has to stay clean. The product has to feel like a choice, not like the output of a solved optimization problem.

The best PMs in this environment won’t be the ones with the most innovative ideas. They’ll be the ones who can convert material cost chaos into coherent customer-facing decisions.

They’ll be the ones who understand their supply curve as intimately as their user curve. They’ll be the ones who can look at a memory vendor’s capacity roadmap and see the three product moves they’re now required to make before they even start thinking about features.

And there’s no going back until either memory gets cheap again, or every company gets as much supply leverage as Apple. Spoiler: it will be a very long time before the second thing happens.

What constraint is currently reshaping your product roadmap? The ones we see are always less interesting than the ones we’re still learning to name.

It is said that Apple is going to increase its prices.